As we navigate the financial landscape of 2026, homeowners across Connecticut, from Southington, to Farmington, to Madison, to Guilford are sitting on a valuable resource: their home equity. With property values maintaining strength in Connecticut, a cash-out refinance has become a strategic tool for financial management. This mortgage option allows you to replace your current loan with a larger one, giving you the difference in cash.

At New England Home Mortgage (NEHM), we see clients utilizing these funds to transform their financial futures. Whether you are looking to modernize your home, consolidate high-interest debt, help pay for college, or expand your investment portfolio, understanding how to effectively unlock this capital is key. Our team, led by Brian Taylor, focuses on a "people-first" approach, ensuring you get a loan structure that aligns with your long-term goals.

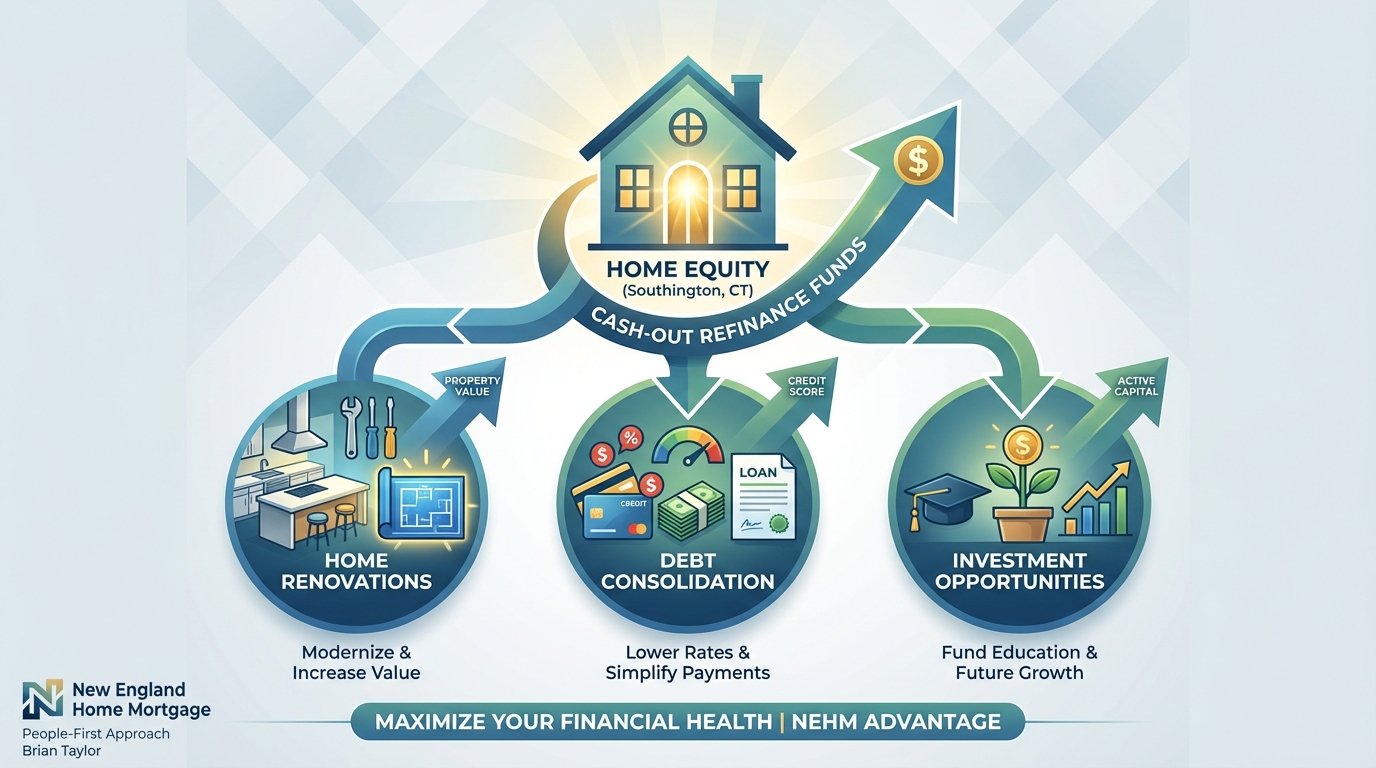

Deciding how to use your equity is a personal decision, but some strategies offer higher returns than others. Here are the most popular ways our Southington clients are utilizing cash-out refinancing in 2026:

Consulting with a local expert like Brian Taylor at NEHM can help you determine which path maximizes your financial health.

Choosing the right lender is just as important as choosing the right loan. New England Home Mortgage has been serving the Southington community, and towns all across Connecticut, with a commitment to trust and communication. We streamline the loan process to make it stress-free, from pre-qualification to closing.

Our team understands the local Connecticut market nuances. We take the time to analyze your specific financial situation—whether you are a first-time refinancer or a seasoned investor. By offering personalized advice and competitive rates, we help you secure a future where your home works for you.

Ready to explore your options? You can reach Brian Taylor directly at (860) 798-7289 or email brian@brianct.com to start the conversation.

Q1: What is the limit on how much cash I can take out?

Typically, lenders allow you to borrow up to 80% of your home's current appraised value.

Q2: How does a cash-out refinance differ from a HELOC?

A cash-out refinance replaces your existing mortgage with a new one, usually with a fixed rate, whereas a HELOC is a separate line of credit with a variable rate.

Q3: Are there closing costs associated with a cash-out refinance?

Yes, similar to your original mortgage, there are closing costs (appraisal, origination fees, etc.), which can often be rolled into the loan amount. However there are advantages to refinances that offset a majority of these costs.

Q4: Is the interest on a cash-out refinance tax-deductible?

Interest may be tax-deductible if the funds are used to buy, build, or substantially improve your home. Consult a tax professional for advice specific to 2026 tax laws.

Q5: How long does the process take with NEHM?

New England Home Mortgage streamlines the process, typically closing loans in under 30 days, depending on appraisal availability and documentation speed.

Click here to contact Brian Taylor and get a free Cash-Out Refinance Quote today!